Table of Contents

Contents are generated from article headings.

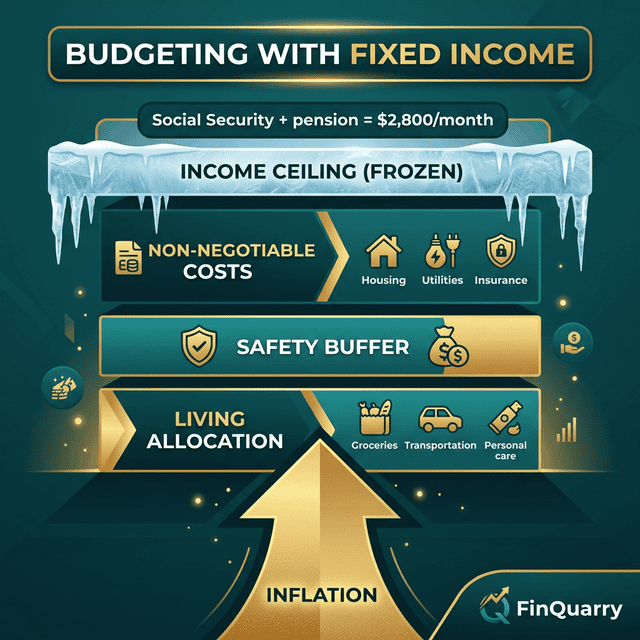

A fixed-income budget is a financial plan designed for income sources that do not increase with effort, hours, or performance — including pensions, Social Security, disability payments, annuities, and salaried positions without overtime or bonus eligibility. Fixed-income budgets operate under an income ceiling that does not respond to rising costs, making every price increase, unexpected expense, and inflation adjustment a direct compression of available spending capacity.

Fixed-income budgeting is structurally distinct from low-income budgeting, though the two frequently overlap. A retiree receiving $3,200/month in combined pension and Social Security has fixed income at a moderate level. A disability recipient receiving $1,400/month has fixed income at a survival level. Both face the same constraint — income does not respond to cost changes — but strategies differ based on the margin between income and essential expenses.

This content discusses budgeting with fixed income using financial planning principles and retirement finance research. Social Security amounts, pension structures, and disability benefits vary by jurisdiction, program, and individual circumstances. FinQuarry provides informational content only — this does not constitute personalized financial advice.

The Core Challenge: Inflation Erosion

How Fixed Income Loses Purchasing Power

Social Security includes a Cost-of-Living Adjustment (COLA), but the CPI used for COLA calculation does not always reflect the specific cost increases fixed-income households experience most: healthcare, prescriptions, and housing.

A person receiving $2,800/month who received a 3.2% COLA gets approximately $89 more per month. But if their prescription costs increased by $45, rent by $75, and utilities by $30, the actual increase is $150 — leaving a $61/month gap. Over five years, these gaps compound: the budget that worked initially becomes progressively tighter without any change in spending behavior. The money did not shrink. The costs outgrew it.

What Cannot Be Compressed Further

In many fixed-income budgets, essential expenses already consume 80–90% of income. Compressible categories (dining, entertainment, subscriptions) are typically already minimal. When budget failure occurs on fixed income, it is usually not overspending on wants — it is needs expanding beyond coverage.

Fixed-Income Budget Architecture

Layer 1: The Non-Negotiable Layer

Medical costs, prescriptions, housing, basic food, insurance, and utilities must be funded first — every month, without exception. Calculate precisely from actual costs, update quarterly, and auto-pay where possible to avoid late fees that consume already-scarce margin.

A person on $2,800/month might have $2,240 in non-negotiable costs: housing ($850), utilities ($180), prescriptions ($220), food ($450), insurance ($290), medical co-pays ($100), transportation ($150). This consumes 80% of income — leaving $560 for everything else.

Layer 2: The Safety Layer

Even on fixed income, $25–50/month directed to an emergency buffer prevents individual crises from cascading. $25/month produces $300/year. $50/month produces $600/year. These numbers are small by conventional standards but significant in context — they represent the difference between absorbing a $400 car repair from savings and absorbing it on a credit card at 22% APR.

Layer 3: The Living Layer

A budget eliminating all discretionary spending maximizes margin but is psychologically unsustainable. A small living allocation — $30–75/month — provides permission to spend without guilt and makes the budget’s restrictions tolerable long-term.

Cost Reduction Strategies

Assistance Program Audit

Many fixed-income households are eligible for programs they are not enrolled in. A systematic audit often identifies $100–300/month in cost offsets:

- Utility assistance: LIHEAP provides heating/cooling bill assistance for qualifying households

- Prescription assistance: Medicare Extra Help/Low-Income Subsidy covers Part D costs

- Property taxes: Senior exemptions reduce property tax burden in most states

- Food assistance: SNAP provides monthly food benefits based on income

- Phone/internet: Lifeline program and Affordable Connectivity Program provide service discounts

The Benefits.gov benefits finder identifies federal and state programs by location and circumstance.

Service Renegotiation

Insurance premiums, phone plans, and internet service can often be reduced through competitive shopping. On fixed income, saving $40/month on car insurance and $25/month on internet produces $780/year — meaningful margin redirectable to the safety or living layer.

Healthcare Cost Optimization

For Medicare recipients, annual plan comparison during Open Enrollment (October 15–December 7) can reduce prescription and premium costs. Plans change formularies and pricing annually. The Medicare Plan Finder provides personalized plan comparison.

Handling Unexpected Expenses on Fixed Income

The primary defense is the safety layer accumulation. The secondary defense is a clear priority hierarchy: medical necessities first, housing second, food third, utilities fourth. Non-essential items are the first suspended when an unexpected cost arrives.

The third defense is knowing assistance resources before the emergency — local emergency financial assistance, nonprofit organizations, and community support — so the response is a phone call, not a frantic search.

Is Saving Possible on Fixed Income?

Saving on fixed income requires structural commitment rather than hopeful intention. A pay-yourself-first approach — $25 transferred to savings on income day — builds $300/year. Over 36 months, $900. Small relative to conventional advice but significant in context: any buffer represents the difference between absorbing a disruption and being destabilized by one.

When Fixed Income Genuinely Cannot Cover Essentials

When essential expenses exceed fixed income — calculated from actual costs, not estimates — no budgeting technique closes the gap. The issue is structural and requires structural intervention: housing assistance, Medicaid enrollment, food assistance, nonprofit credit counseling, or evaluating additional income possibilities. Acknowledging this reality is accurate diagnosis, not failure.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry