Table of Contents

Contents are generated from article headings.

Budgeting guilt is an emotional response where a person feels anxiety, shame, or self-criticism after spending money — even when the purchase falls within a funded budget category. Budgeting guilt operates independently of actual financial behavior: a person who budgeted $50 for discretionary spending, spent $6 on coffee within that allocation, and experienced guilt has made a planned, budgeted expenditure that the emotional system categorized as irresponsible.

Financial guilt does not improve financial outcomes. Research in behavioral economics indicates that guilt erodes budget sustainability by making the system emotionally punishing even when functioning as designed. The person who feels guilty every time they spend — even within budget — eventually abandons the budget not because it failed, but because following it feels worse than not following it.

This content discusses the psychological dimensions of budgeting guilt using behavioral economics, financial psychology research, and financial planning principles. Individual emotional responses to money are shaped by personal history, culture, and economic context. FinQuarry provides informational content only — this does not constitute personalized financial advice.

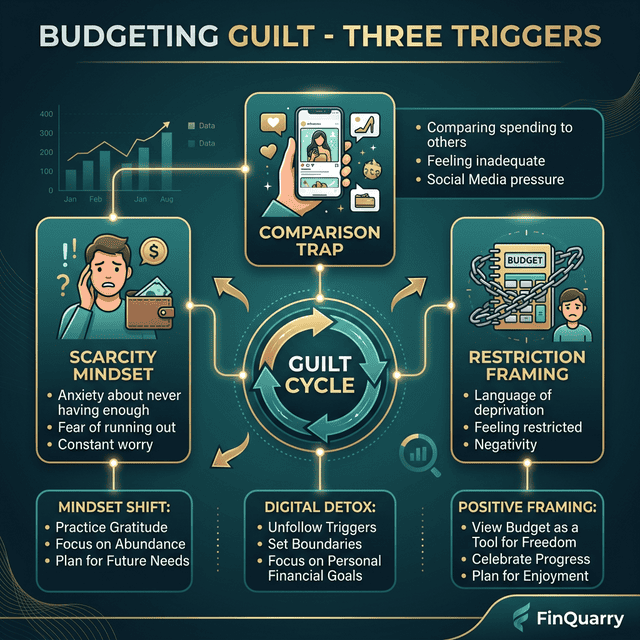

Three Mechanisms That Create Budgeting Guilt

The Scarcity Mindset Inheritance

Many adults inherited a relationship with money defined by scarcity — from childhood financial instability, from parents who communicated financial stress, or from communities where spending equaled irresponsibility. This inherited mindset treats every discretionary purchase as a potential threat.

A person raised in a household where a $20 dinner triggered visible parental stress may feel that same stress response at age 35, earning $5,500/month with $200 budgeted for dining — because the emotional coding (“spending is dangerous”) persists independently of current financial reality. The $6 coffee does not trigger guilt because of budget math. It triggers guilt because of encoded belief.

The Comparison Trap

Financial success narratives on social media create implicit comparison frameworks. Someone saved 40% of income. Someone retired at 35. Against these curated benchmarks, spending $6 on coffee feels like failure — not because the purchase was harmful but because the comparison suggests the person should be doing more, faster, with less enjoyment.

These comparisons ignore income disparity, cost-of-living differences, and the fact that curated narratives omit messy realities. But cognitive biases widen the perceived gap by making others’ success appear more uniform than it actually is.

The Restriction Framing

Financial advice that frames budgeting as sacrifice (“cut this, eliminate that, deny yourself now”) positions every expenditure as a concession. Under this framing, spending within budget still feels like failure because the budget’s limits are treated as minimums (“at least stay under”) rather than permissions (“the budget says this is okay”).

Restructuring the Budget for Guilt-Free Operation

The Permission Category

The most effective structural intervention is a dedicated “permission money” category — a funded allocation for discretionary spending that requires no justification, no sub-category tracking, and no guilt. This is not optional. It is an architectural requirement.

A person who budgets $100/month labeled “guilt-free spending” and buys a $6 coffee is making a complaint expenditure within a designed allocation. The psychological shift: from transgression (“I shouldn’t have”) to compliance (“this is exactly what this money is for”). A budget without fun money is structurally incomplete.

The “Already Saved” Mental Model

Before any discretionary spending occurs, the savings allocation has already left the account. Money remaining in the spending account has already passed through the savings filter — it is, by definition, money the budget designated for spending.

A person with $4,000 take-home who auto-transfers $400 to savings and $200 to debt sees $3,400 in their spending account. Every dollar in that $3,400 is budgeted spending money. Using it is not draining savings — it is fulfilling the budget’s design.

Separating Net Worth From Self-Worth

Financial guilt often stems from conflating savings balance with personal value. Once savings transfers are automated and funded, the savings balance performs its function without emotional monitoring. The person’s job is living within the remaining budget — including discretionary spending — without treating the savings balance as a moral scorecard.

When Guilt Is Actually a Signal

Misaligned Spending

If a purchase triggers guilt because it conflicts with the person’s own values — not society’s values, not financial advice’s values — the guilt is diagnostic. It suggests the spending was impulsive or the category allocation does not reflect genuine priorities. This is worth examining through category reallocation.

Budget Boundary Violations

Guilt after spending money allocated to savings, debt, or another committed category is functionally appropriate — it signals that a budgeted boundary was crossed. The response: examine whether the boundary was realistic, and adjust if needed.

Repetitive Pattern Recognition

Guilt that surfaces repeatedly around the same purchase type — online shopping, convenience food, impulse subscriptions — may indicate a spending pattern the person genuinely wants to change. This connects to emotional spending patterns rather than budget permission structure.

Practical Guilt-Reduction Strategies

The 24-Hour Guilt Test

When guilt follows a budgeted purchase, wait 24 hours. If guilt persists and the purchase feels misaligned, adjust. If guilt dissipates (the usual outcome), it was emotional noise rather than financial signal.

The Category Confidence Audit

Review every budget category and assess: “Do I feel confident this amount is appropriate?” Categories producing anxiety when spent are under-allocated, over-scrutinized, or carrying psychological weight they should not. Even slight upward adjustment reduces guilt across the entire budget.

Celebrate Compliance, Not Just Savings Growth

Redefining success from “saved the most this month” to “followed the plan this month” changes the emotional reward structure. Living within a sustainable budget is a harder achievement than maximizing a savings number — and deserves recognition.

Is Budgeting Guilt More Common Among Certain Groups?

Research suggests budgeting guilt is more prevalent among first-generation savers, women (who face stronger cultural messaging about financial caution), and people from financially unstable households. These groups carry a higher baseline of financial anxiety that the act of spending activates regardless of budget compliance. Acknowledging that guilt is culturally loaded — not universally rational — is the first step toward separating appropriate financial feedback from inherited emotional patterns.

When Professional Support Is Needed

When budgeting guilt prevents any discretionary purchases, produces anxiety about opening bank statements, or drives compulsive saving that damages quality of life, the issue has moved beyond budgeting into financial anxiety disorder. Financial therapists specialize in the intersection of money and emotional health — a budget can be perfectly designed, but when guilt makes it unlivable, the needed intervention is psychological, not financial.

Written by Marcus Tremblay, Senior Financial Analyst | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry