Table of Contents

Contents are generated from article headings.

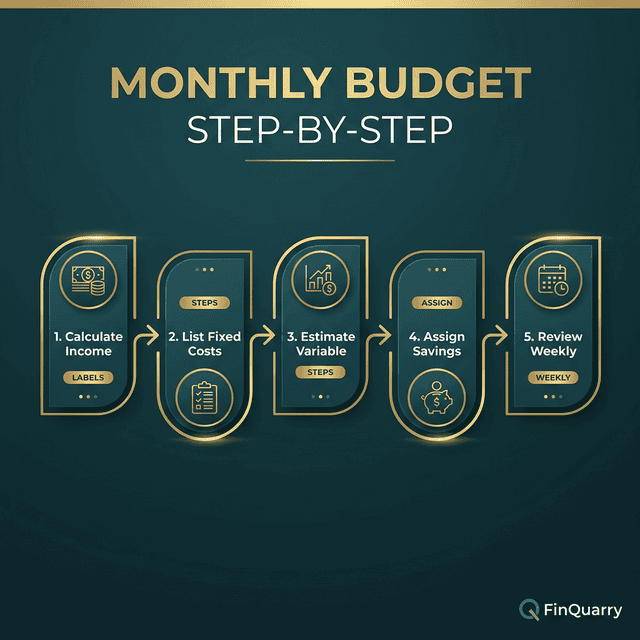

A monthly budget is a structured income-allocation system that assigns every dollar of after-tax pay to a specific spending category, savings target, or debt obligation across a single calendar month. Monthly budgeting operates through a five-step sequence — calculating real income, mapping fixed costs, planning variable spending, automating savings, and reviewing results — where each step builds on the previous one to create a financial architecture that functions with minimal daily decision-making.

Monthly budgets fail most often not from overspending but from structural errors in the design phase. A budget built on gross income instead of take-home pay, estimated expenses instead of audited actual costs, or willpower instead of automation tends to collapse by the third week. The sequence in which a budget is built determines whether it survives the full month.

This content discusses monthly budgeting processes using financial planning principles recognized by the Consumer Financial Protection Bureau and behavioral economics research. Costs, income levels, and financial products vary by jurisdiction. FinQuarry provides informational content only — this does not constitute personalized financial advice.

Step 1: Calculate Your Real Take-Home Number

The real take-home number is the amount that arrives in a bank account after taxes, insurance premiums, retirement contributions, and payroll deductions are removed. Every budget category must be built from this number — not gross pay, not salary, not quoted compensation.

Why Gross Income Budgets Fail Immediately

A budget built on gross income contains a mathematical error before any spending occurs. A person earning $5,000 gross with a $3,800 take-home has $1,200 of phantom allocation — categories funded on paper with money that never reaches the checking account. This gap between perceived income and actual income is where the first budget failure originates.

For example, a household budgeting $1,500 for rent against $5,000 gross sees a 30% housing ratio. Against the actual $3,800 take-home, that same rent consumes 39.5% — a structurally different budget that leaves $500 less for all other categories than the gross-income version predicted.

Handling Variable Take-Home Pay

Workers with overtime, commissions, tips, or gig income face fluctuating take-home numbers. The structural solution is budgeting from the income floor — the lowest reliable month of the past six.

A freelance graphic designer who earned $3,200, $4,800, $3,600, $5,100, $3,400, and $4,200 over six months builds the budget on $3,200. Anything above the floor is allocated after arrival. This prevents dependence on income that may not materialize, which is the core failure point of irregular income budgeting.

Step 2: Map Your Fixed Obligations First

Fixed obligations are payments that occur regardless of how the month goes — rent or mortgage, utilities, insurance, minimum debt payments, car payments, phone, and internet. These form the budget’s foundation layer and are non-negotiable in the short term.

The 72-Hour Bill Audit

Instead of estimating fixed costs from memory, pull three months of bank and credit card statements, highlight every recurring charge, and total them. Most people discover 2–4 forgotten recurring payments during this audit — streaming services from old trials, auto-renewed memberships, unused software subscriptions.

A typical audit reveals $40–120 per month in charges that can be eliminated before the budget begins. One case: a family discovered three overlapping streaming services ($42/month), a gym membership no one used ($35/month), and an expired software trial ($9.99/month) — a total of $86.99/month recovered with three cancellation calls.

Separating Fixed From Semi-Fixed

True fixed costs remain constant (rent, loan payments). Semi-fixed costs vary within a predictable range — electric bills, gas, water. The budget should use the three-month average for semi-fixed costs and add a 10% buffer.

If electric bills over three months were $140, $165, and $155, the average is $153. The budgeted amount should be $168 (average + 10%). This buffer prevents a high-usage month from breaking the budget mid-month.

Step 3: Build the Variable Spending Plan

After fixed obligations are subtracted from take-home income, the remaining number is the variable spending pool — money available for groceries, transportation, personal care, entertainment, clothing, and discretionary purchases. Variable spending lacks natural boundaries unless the budget creates them.

Category Allocation by Actual Data

The critical mistake is allocating variable spending based on aspirational targets rather than actual behavior. Pull variable spending data from the same three-month audit.

A person spending $650 monthly on groceries who budgets $500 has created a realistic adjustment. Budgeting $300 creates a deprivation gap that triggers budget abandonment. Reduce categories by 15–20% maximum from the audited baseline — reductions beyond 25% rarely sustain past three weeks.

The Fun Money Line Item

A monthly budget without designated discretionary spending typically survives three weeks. Planned fun money — a specific, pre-allocated amount for enjoyment without tracking or justification — functions as the psychological pressure valve.

Research on financial self-regulation indicates that planned indulgence reduces unplanned overspending by removing the deprivation trigger. A person who allocates $80/month for “guilt-free spending” and uses it is making a budgeted expenditure. A person without that category who spends $80 spontaneously experiences guilt disproportionate to the identical dollar amount — because one was planned and the other was not.

Step 4: Automate the Savings Layer

Savings should leave the checking account on payday — before any variable spending occurs. Treating savings as the first transfer rather than the leftover converts saving from a willpower exercise into an automatic structural process.

The Pay-Yourself-First Transfer

On the day income arrives, an automatic transfer moves the savings allocation to a separate account. Even $50 per month qualifies — the amount matters less than the automation.

The checking account then displays only spendable money, replacing the false visual of a full balance that leads to unnoticed overspending. A person with $3,800 take-home who auto-transfers $200 to savings sees $3,600 as their available balance — and spends accordingly.

Where to Start If Savings Feels Impossible

When the gap between income and expenses leaves no room for savings, the budget’s function shifts from allocation to diagnosis. The monthly budget reveals exactly which categories consume income and identifies where reduction produces real margin.

Compressible spending often hides not in obvious categories (housing, debt) but in accumulated small charges — subscriptions ($40), delivery fees ($35), convenience charges ($25), impulse purchases ($50) — totaling $150 per month yet invisible without the budget making them visible.

Step 5: Build the Monthly Review Ritual

A monthly budget is a feedback system, not a static document. Each month’s actual spending data produces a more accurate budget for the following month.

The 30-Minute Month-End Review

Within three days of month-end, compare actual spending to planned spending in every category. Which categories exceeded allocation? Which came in under? Were there uncategorized expenses?

A person who budgeted $500 for groceries and spent $540 three months running does not have a discipline problem — they have a calibration problem. The budget should be adjusted to $550, with another category reduced to compensate. This iterative calibration is how budgets improve through data, not willpower.

Adjusting Without Starting Over

When a category consistently exceeds its allocation, adjusting the allocation produces better outcomes than demanding behavioral change the person cannot sustain.

The most common reason people feel their budget never works is restarting with the same unrealistic numbers each month instead of calibrating to observed spending patterns. A $50 adjustment to one category — funded by a $50 reduction in another — often resolves months of budget frustration in a single revision.

Is It Better to Budget Weekly or Monthly?

Monthly budgeting captures the full income-to-expense cycle, which aligns with how most fixed obligations bill. Weekly budgeting within the monthly framework — dividing variable spending into four weekly allocations — reduces the psychological weight of managing an entire month at once.

A $1,200 monthly variable spending pool divided into four $300 weekly segments provides a natural checkpoint every seven days. This approach works particularly well for people who find a full month’s budget abstract and difficult to track.

What If My Budget Does Not Balance After Following These Steps?

A budget that remains negative after all five steps has produced its most valuable output — an honest picture of a structural income-expense gap. When income minus fixed obligations minus minimum variable spending minus minimum savings equals a negative number, no budgeting technique closes the gap.

This is diagnostic, not failure. The next step shifts from budget optimization to income restructuring (raise negotiation, additional work, career development) or obligation reduction (housing downsize, debt consolidation, insurance renegotiation).

How Long Does It Take for a Monthly Budget to Start Working?

A monthly budget typically requires three complete cycles before stabilizing. Month one produces raw data and likely overshoot in multiple categories. Month two produces the first meaningful calibrations. Month three produces a budget that approximately matches actual spending.

By month four, most people report the budget transitions from conscious effort to financial habit — an automatic background process rather than daily decision-making. The key is surviving the first two months without expecting precision.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry