Table of Contents

Contents are generated from article headings.

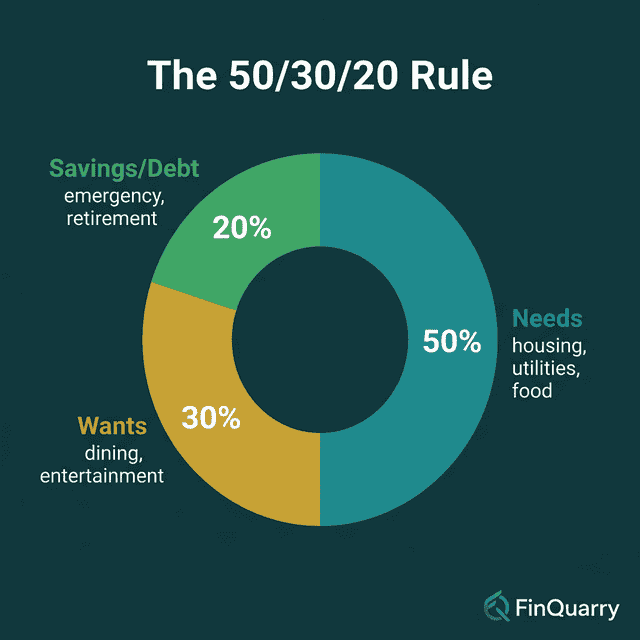

The 50/30/20 rule is a percentage-based budgeting framework that divides after-tax income into three categories: 50% for needs (essential living costs), 30% for wants (discretionary spending), and 20% for savings and debt repayment. Senator Elizabeth Warren and her daughter Amelia Warren Tyagi popularized this framework in the 2005 book All Your Worth, and it remains one of the most widely recommended entry-level budgeting methods in personal finance.

The 50/30/20 rule trades granular control for simplicity. It does not track individual transactions or require category-level monitoring. Instead, it provides three broad guardrails that keep spending in proportion to income — which produces adequate financial outcomes for most stable-income households with significantly less effort than methods like zero-based budgeting.

This content discusses the 50/30/20 budgeting framework using financial planning principles. Income levels, housing costs, and cost-of-living vary by jurisdiction. FinQuarry provides informational content only — this does not constitute personalized financial advice.

How the 50/30/20 Split Works

Each percentage represents a maximum allocation target, not a fixed requirement. The categories function as spending ceilings that the budget aims to stay within or below.

The 50% Needs Category

Needs are essential expenses required for basic functioning: housing (rent or mortgage), utilities, groceries, health insurance, minimum debt payments, transportation to work, and childcare required for employment. For a person earning $4,000/month after taxes, the needs ceiling is $2,000.

A practical test for classifying needs: if eliminating the expense would create immediate hardship or legal consequence, it qualifies as a need. Netflix does not qualify. Electricity does. A gym membership does not. Health insurance does.

The 30% Wants Category

Wants are discretionary expenses that improve quality of life but are not essential for survival or legal compliance: dining out, entertainment, streaming services, hobby spending, vacations, clothing beyond functional necessity, and upgraded versions of needs (choosing a $1,400/month apartment when a $1,100 option meets requirements).

For the same $4,000 income, the wants ceiling is $1,200. This category often produces guilt in budget-conscious people — but budgeting without guilt requires accepting that wants are legitimate, funded allocations within the plan.

The 20% Savings and Debt Category

Savings and accelerated debt repayment together receive at least 20% of after-tax income. For $4,000 income, this is $800/month. This category funds emergency savings, retirement contributions beyond employer match, extra debt payments above minimums, and goal-directed savings (vacation fund, home down payment).

Research from the Consumer Financial Protection Bureau indicates that households maintaining a 20% savings rate for 5+ years accumulate emergency reserves and retirement readiness significantly faster than households without structured savings targets.

Where the 50/30/20 Rule Works Best

Stable Income Households

The 50/30/20 rule performs best when income is predictable and needs consume less than 50% of take-home pay. A dual-income household earning $7,000/month after taxes with $3,200 in fixed costs (45.7% needs) has a clean 50/30/20 fit: $3,500 needs ceiling, $2,100 wants ceiling, $1,400 savings minimum.

Financial Beginners

People new to budgeting benefit from the 50/30/20 rule because it requires no category-level tracking. The only monitoring needed is whether each of the three groups stays within its percentage — a assessment that takes 5–10 minutes weekly using bank statements alone.

Where the 50/30/20 Rule Breaks Down

High-Cost-of-Living Areas

In cities where median rent consumes 35–45% of income, needs alone can exceed 50% before any other essential is counted. A person earning $3,500/month with $1,400 rent (40%) plus $200 utilities, $400 groceries, $150 insurance, and $200 minimum debt payments (needs total: $2,350 = 67%) cannot mathematically achieve the 50% target.

This does not mean the rule is useless — it means the person must adjust the percentages to fit their reality (perhaps 65/20/15) rather than treating the rule as a pass/fail test.

Below-Median Income

Households earning below area median income generally spend 60–80% on needs, leaving 20–40% for both wants and savings combined. The 50/30/20 rule, designed for median and above-median incomes, produces frustration and shame when applied to incomes where the math cannot balance. Fixed income budgeting addresses this constraint directly.

Debt-Heavy Situations

A person allocating 20% to savings while carrying $15,000 in 22% APR credit card debt is mathematically suboptimal — the debt interest ($3,300/year) exceeds likely savings returns ($500–750/year at 4–5% APY). In debt-heavy situations, temporarily adjusting to 50/20/30 (with 30% to debt) produces faster financial improvement.

How to Apply the 50/30/20 Rule in Practice

Step 1: Calculate After-Tax Income

Use actual take-home pay from the most recent pay stub, not salary or gross pay. Include all regular income sources.

Step 2: Calculate the Three Ceilings

Multiply take-home by 0.50, 0.30, and 0.20 to set each category’s maximum.

Step 3: Classify Current Spending

Review three months of bank and credit card statements. Total all needs-category spending, all wants-category spending, and all savings/debt payments. Compare actuals to the three ceilings.

Step 4: Adjust the Largest Variance

If needs exceed 50%, examine housing costs and recurring obligations for reduction opportunities. If wants exceed 30%, identify the largest wants subcategory and consider temporary reduction. If savings falls below 20%, automate even a small monthly transfer and increase it quarterly.

Can I Modify the 50/30/20 Percentages?

Modifying the percentages is expected — the rule provides a starting framework, not a rigid formula. Common effective modifications include:

60/20/20 — for high-cost-of-living areas where needs genuinely consume more than half of income.

50/20/30 — for aggressive debt repayment phases where the savings/debt category needs temporarily increased allocation.

40/30/30 — for high-income households where needs consume less than 40%, freeing additional capacity for savings and discretionary enjoyment.

The percentages should reflect the person’s actual financial structure. Forcing a 50/30/20 split onto a financial life that naturally doesn’t fit produces the kind of artificial constraint that causes budget abandonment.

How Does the 50/30/20 Rule Compare to Other Methods?

The 50/30/20 rule prioritizes sustainability over precision. Compared to zero-based budgeting (which assigns every dollar), the 50/30/20 rule provides less visibility but requires far less effort. Compared to envelope budgeting (which uses physical cash), it requires no cash handling but provides weaker spending friction.

For a detailed comparison of how each budgeting method balances effort, control, and sustainability, see our budgeting methods overview.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry